Unemployment rates are low, and inflation appears to be falling, yet consumer sentiment remains unexpectedly low. While traditional measures like the Consumer Price Index (CPI) may suggest inflation is low, a closer look reveals a different story. Economists, who typically rely on unemployment and official inflation rates to gauge consumer sentiment (the misery index), have been surprised by this discrepancy. However, it all unravels when you include borrowing costs like interest rates and other borrowing fees. These costs have surged at rates not seen in decades- and Americans are feeling it.

March 2024 inflation numbers came in at 3.5%, down significantly from its peak of 9.1% in June 2022. Poll after poll show that Americans are increasingly concerned about the rising cost of living, a pivotal issue in the Presidential election. The Biden White House are touting the success of “Bidenonomics,” citing low unemployment and inflation. The media is framing this discrepancy as a vibesession, “a recession experienced not in rising costs of living or growing unemployment but in vibes.” In short, telling Americans everything is great, your cost of living is imaginative.

However, the disconnect between these official figures and the lived experiences of many Americans reveals a significant oversight: the cost of borrowing. In a recent report, Economist Larry Summers, a Democrat and former alum of the Obama and Clinton white House, has shed light on this discrepancy by highlighting that inflation is substantially higher when the cost of money is considered.

Traditional Price Indexes like CPI does not factor the cost of money (borrowing) into its formula for inflation. Summers report shows that the lows in US consumer sentiment are strongly correlated with borrowing costs and consumer credit supply. Americans concerns over borrowing costs have reached levels not seen since the Jimmy Carter era.

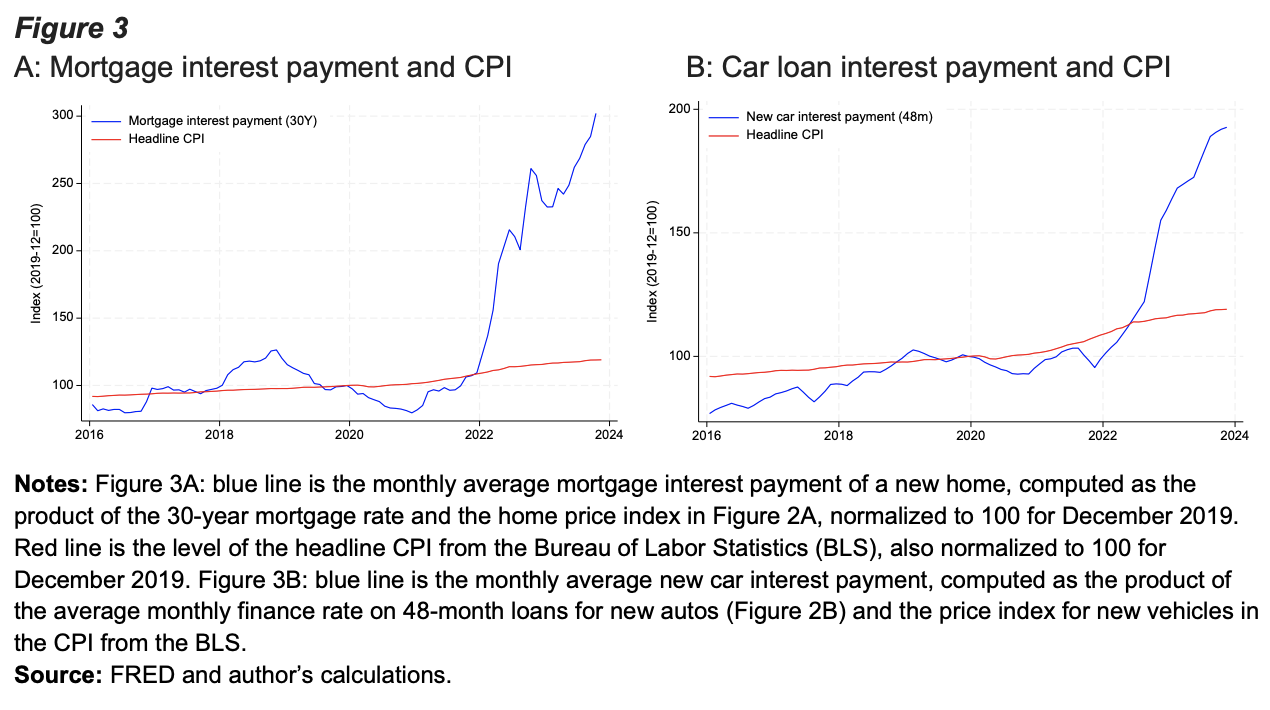

The result- a disconnect between official inflation figures and the inflation that consumers experience in their daily lives. Specifically, the report highlights what is left out of the government inflation numbers:

“the growth of interest rates for mortgages or car loans and the willingness of banks to extend consumer installment loans… which included a measure of the cost of homeownership which reflect mortgage payments…the market for auto loans and personal interest payments in consumption to propose proxies that better reflect the actual costs borne by consumers. The cost of financing car purchases is absent from the official price indices (CPI).”

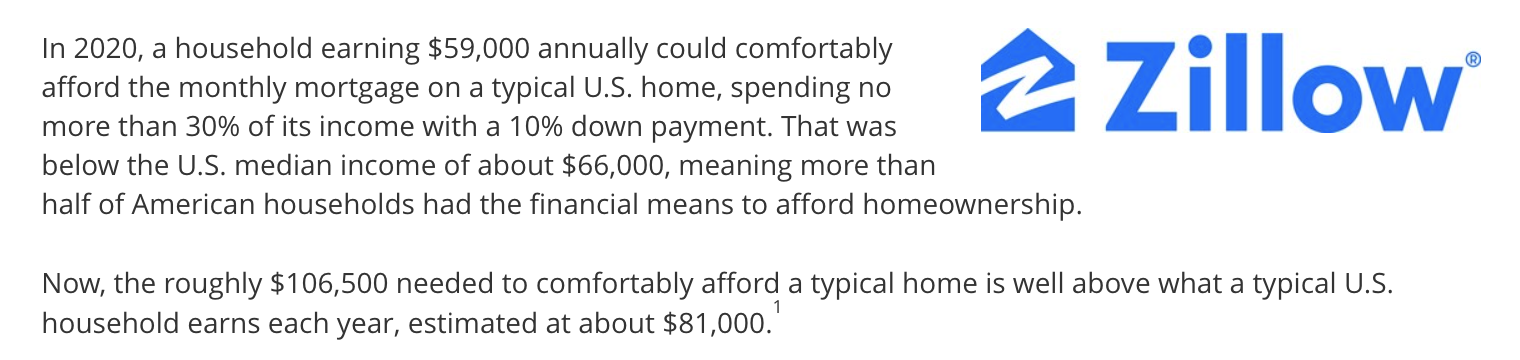

We all know this to be true if you’re trying to buy a house, a car or take out a loan. Compare the cost of taking out a mortgage on a home and compare it from 2020 to now. You now need to make 80% more and while prices on the average home have risen 23%.

Source: Zillow

To get a more accurate picture of real inflation and the effect Americans are feeling regarding the cost of living, we need to create alternative measures of inflation that include borrowing costs, rather than relying solely on traditional measures of inflation like the CPI. And it’s time for the Biden White House to stop telling you things are getting better and inflation is on the decline- because it is not, and Americans know it.

{kind=link}